The Freight Market Is Finally Cleaning House, and Enforcement Is Holding the Broom

Summary: After the longest freight recession in modern history, the rebound that emerges may be unlike any before it: driven not by a surge in demand, but by the systematic removal of those who never should have been in the market to begin with.

The freight market is turning. After 13 consecutive quarters of margin compression, carrier exits, and rate floors that never quite held, something different is happening entering 2026. Capacity has contracted to levels not seen since before the post-pandemic boom. Spot rates are tracking materially higher year-over-year. And for the first time in the history of this industry, there is a credible case that the recovery, if it arrives in full, will be driven primarily by supply-side contraction, not a surge in demand.

That is worth sitting with for a moment. Every previous freight market tightening in living memory was demand-led: consumer spending surges, inventory restocking, manufacturing rebounds. This time, the capacity has been removed. The trucks are exiting. And a meaningful share of that exit is not organic market discipline. It is enforcement. Regulators on both sides of the U.S. and Canadian border are, finally, doing the job the industry has begged them to do for a decade.

This is a good thing. A very good thing. And it is long overdue.

A Heavily Regulated Industry With Almost No Enforcement

Trucking is one of the most regulated industries on the continent. Hours of service. Weight limits. Insurance minimums. Drug and alcohol testing. CDL standards. ELD mandates. Employment law. Tax compliance. The regulatory framework is extensive, deliberately so, because the stakes are high. A Class-8 Tractor and 53’ Trailer combination operated by an unqualified, fatigued, or uninsured driver is not a business risk. It is a public safety catastrophe waiting to happen.

And yet, measured against the sheer number of market participants, tens of thousands of carriers and brokers operating across North America, the enforcement of those regulations has been, for decades, almost nonexistent relative to scale. The good operators, the ones who carry proper insurance, who employ their drivers correctly, who maintain their equipment, who pay their taxes, have been competing against a shadow industry that operates under none of those constraints.

They follow the law. They absorb the cost. And they watch their margins erode in a race to the bottom driven by actors who are not playing by the same rules.

Trucking has always been a heavily regulated industry. The problem was never the rules. It was the absence of anyone willing to enforce them at scale. The good ones suffered. The bad actors moved through this industry like a cancer.

This is not a minor inefficiency. It is a structural imbalance that has warped pricing, suppressed wages, degraded safety, and rewarded exactly the wrong behavior. Compliant carriers price at cost. Non-compliant carriers price below cost, forcing (externalizing) risk onto the public, and undercut every carrier trying to do things right.

The Free-est of Free Markets – With a Number To Prove It

The U.S. Department of Justice (DOJ) uses the Herfindahl-Hirschman Index (HHI) as its primary tool for measuring industry competitiveness and flagging markets prone to anti-competitive behavior. The scale runs from 0, perfectly competitive, to 10,000, a pure monopoly. Markets below 1,500 are considered unconcentrated. Above 1,800, the DOJ begins scrutinizing mergers for antitrust risk. Above 2,500, markets are classified as highly concentrated.

Truckload trucking is none of those things. Based on published market structure data, more than 580,000 active motor carriers are registered with the Federal Motor Carrier Safety Administration (FMCSA). The top 10 full truckload carriers control roughly 5% of total market revenue, and 97% of carriers operate 20 or fewer trucks.

Consistent with this highly fragmented structure, the estimated HHI for the for-hire truckload sector is approximately 50 to 100 points. That places trucking below the DOJ’s threshold for even cursory antitrust concern and an order of magnitude below the floor for what regulators consider an “unconcentrated” market.

For context: the U.S. parcel market, where UPS and FedEx together hold over 75% of market share, carries an estimated HHI above 3,600, well into “highly concentrated” territory and a market the DOJ monitors closely. Class I rail, where seven carriers control roughly 70% of all traffic, sits above 2,000. Trucking, by comparison, barely registers.

The implication is not subtle. In a hyper-competitive market where no single operator can set a price floor, the regulatory floor is the only floor.

Strip away enforcement, and you have not created a free market. You have created an unregulated one. Those are not the same thing. And for over a decade, that is precisely what existed.

Driver Inc. – A Canadian Name for a North American Problem

In Canada, the most visible manifestation of this regulatory vacuum has a name: Driver Inc. The term was coined by Shawn Baird, founder and CEO of Sharp Transportation Systems in Cambridge, Ontario, a mid-sized, compliance-first carrier that has spent years doing the opposite of what Driver Inc. enables.

In November 2018, Baird launched driverinc.ca, a resource website designed to make drivers aware of their rights before incorporating under carrier pressure. It was an early act of industry advocacy from an operator who had watched the model spread and understood exactly what it was costing legitimate carriers.

The model works like this: A carrier classifies its drivers as independent contractors operating through personal incorporated entities, Personal Service Businesses (PSBs), rather than as employees. On paper, it appears to be a legitimate business arrangement.

In practice, when drivers are operating company-owned equipment on company-assigned routes under company direction, they are employees by any reasonable legal definition. The misclassification strips them of employment protections, eliminates payroll tax obligations for the carrier, and allows the operator to submit bids that no compliant competitor can match.

Although “Driver Inc.” as a label is distinctly Canadian, elevated to a major federal policy issue by the Canadian Trucking Alliance, debated in Parliament, and addressed in successive federal budgets, the underlying practice is equally illegal on both sides of the border.

In the United States, the IRS and Department of Labor apply nearly identical standards to distinguish genuine independent contractors from misclassified employees. The economic logic is the same: A driver operating a company truck, on company-defined routes, under company dispatch, is not an independent contractor under U.S. law any more than under Canadian law.

Chameleon Carriers: The American Mirror Image

South of the border, a functionally identical cancer has operated under a different name. Chameleon carriers, companies that accumulate safety violations, shut down, and re-emerge under a new DOT number with a clean record, have been on the FMCSA’s radar for decades. The agency built a prototype detection system, ARCHI, following congressional direction in 2012. And yet the problem persisted, because the regulatory architecture made it too easy to disappear and reappear.

The human cost is documented. GAO (Government Accountability Office) analysis found crashes involving carriers with chameleon characteristics resulted in 217 fatalities and 3,561 injuries over a five-year period. They are approximately three times more likely to be involved in serious crashes than legitimate new-entrant carriers.

They operate with inadequate insurance, fail safety inspections at higher rates, and hire unqualified drivers, sometimes from fraudulent CDL schools certifying operators who have never been properly trained. When caught, they simply incorporate again under a new name with a P.O. box for an address.

Transportation Secretary Sean Duffy and FMCSA Administrator Derek Barrs have escalated this to a stated priority. The FMCSA’s new MOTUS registration system, a full replacement of a 40-year-old infrastructure, is designed to close the front door: requiring verified physical locations, strengthening identity vetting at registration, and integrating compliance history across affiliated entities so a DOT number cannot be laundered by simply changing the sign on the truck door.

The SAFE Act, introduced in February 2026, directs FMCSA to build advanced automation tools to detect chameleon carrier applications at the point of registration. The parallel with Driver Inc. is exact: the same regulatory gap exploited, the same predatory pricing, the same public safety exposure, and now, finally, the same enforcement response.

English Language Proficiency: A Safety Standard That Existed on Paper Only

The English Language Proficiency requirement for commercial drivers is not a new regulation. It has been enshrined in federal law for decades, mandating all CDL holders be able to converse with law enforcement, read and respond to highway signage, and complete required documentation in English. What was new, until very recently, was the complete absence of meaningful consequences for non-compliance.

In 2016, the FMCSA issued internal guidance directing inspectors not to place commercial vehicle drivers out of service for ELP violations. That memo effectively neutered the regulation. For nearly a decade, a federal safety standard sat on the books while inspectors were explicitly instructed not to enforce it. Carriers who hired non-English-proficient drivers faced no meaningful penalty. The regulation existed. The compliance did not.

An April 2025 Executive Order reversed course, directing the FMCSA to resume strict enforcement. In response, the Commercial Vehicle Safety Alliance added English Language Proficiency to the North American Standard Out-of-Service Criteria, effective June 25, 2025.

The new enforcement regime is unambiguous: if a driver cannot understand questions from an officer or respond intelligibly, the officer has authority to place that driver out of service immediately. Translation apps are explicitly prohibited. Reliance on a digital tool to communicate basic safety information is grounds for failure. When operating at 65 mph, a driver cannot use a phone to translate a low bridge sign, and the DOT position is that the same standard applies at roadside.

After enforcement commenced, ELP violations surged, with more than 19,000 violations recorded and over 5,000 resulting in out-of-service orders. The supply-side math is not trivial. Combined with non-domiciled CDL restrictions, analysts estimate these enforcement actions could remove between 5% and 12% of CDL holders, between 214,000 and 437,000 drivers, from the active U.S. driver pool over the next two to three years.

This is not a workforce reduction imposed arbitrarily. It is the belated application of a safety standard that should have been enforced all along. FMCSA Administrator Derek Barrs stated the agency’s position plainly:

“The ability to read road signs, understand safety instructions, and communicate effectively, when that standard is applied inconsistently, it creates risk, not only to the public but to the professional drivers operating alongside someone who may not fully understand the critical instructions.”

For compliant carriers who have always hired to the full standard, English proficiency included, this enforcement shift is unambiguously positive. It removes a cost advantage that was built on a safety deficit.

Non-Domiciled CDLs: A Credentialing System Described as “Broken”

The ELP crackdown did not exist in a vacuum. Running parallel, and deeply entangled, is a sweeping federal action targeting the issuance of non-domiciled commercial driver’s licenses, a credentialing category that regulators have described in terms that leave little room for interpretation.

DOT Secretary Sean Duffy called the existing licensing system for non-citizens “absolutely 100 percent broken” and a “national emergency that requires action right now.” The emergency designation was not rhetorical. In September 2025, FMCSA issued an interim final rule, effective immediately, following a nationwide review of state CDL issuance procedures that revealed widespread non-compliance and a troubling series of fatal crashes. FMCSA identified at least five fatal crashes involving non-domiciled CDL holders in the first months of 2025 alone.

The audit findings were damning. California alone had issued more than 60,000 non-domiciled CDLs in the prior year, with an estimated 15,000 done improperly. States had been issuing credentials to individuals whose immigration status provided no legal basis for commercial driving authority, with no federal database check, no in-person verification requirement, and no mechanism to revoke the credential when work authorization lapsed.

Under the new rule, only H-2B, H-2A, and E-2 visa holders are eligible for non-domiciled CDLs. Every issuance and renewal must be verified against federal databases in person, and the renewal period is shortened to the end of the employee’s work authorization or one year, whichever comes first.

The Secure Commercial Driver Licensing Act of 2025, introduced in February, goes further, proposing to restrict CDL eligibility to U.S. citizens, lawful permanent residents, and specific visa holders, and requiring recertification of all current CDL holders.

The federal government has identified this as a structural integrity problem in the credentialing system. David Heller of the Truckload Carriers Association put it plainly:

“Whether it’s entry-level driver training facilities or motor carrier compliance, English language proficiency or non-domiciled CDLs, there is a flavor of enforcement that is coming out of the agency that is certainly welcome, and it is one that we have been asking for, for years.”

Electronic Logging Devices: When the Compliance Tool Becomes the Fraud

Electronic Logging Devices (ELD) were mandated in 2017 with a straightforward purpose: Replace paper logs with tamper-resistant digital records of hours of service. The intent was sound. The implementation contained a fatal flaw. FMCSA allowed ELD manufacturers to self-certify their own compliance with federal technical specifications, with no independent testing, no government audit of device functionality, and no meaningful barrier to re-registration after revocation. The result was predictable.

A shadow market of intentionally non-compliant ELDs emerged, purpose-built to allow carriers to manipulate driver records after the fact. Third-party services, many operating from overseas, began cold-calling motor carriers with offers to “fix” logbooks, add driving time, or erase hours-of-service violations for as little as $30 per week.

CVSA roadside inspection specialists described carriers directing drivers to call in when they ran out of hours, at which point a third party would remotely alter the ELD record to eliminate the violation entirely. In documented cases, records of duty status were shifted back by days, concealing up to 21 hours of actual driving time per trip.

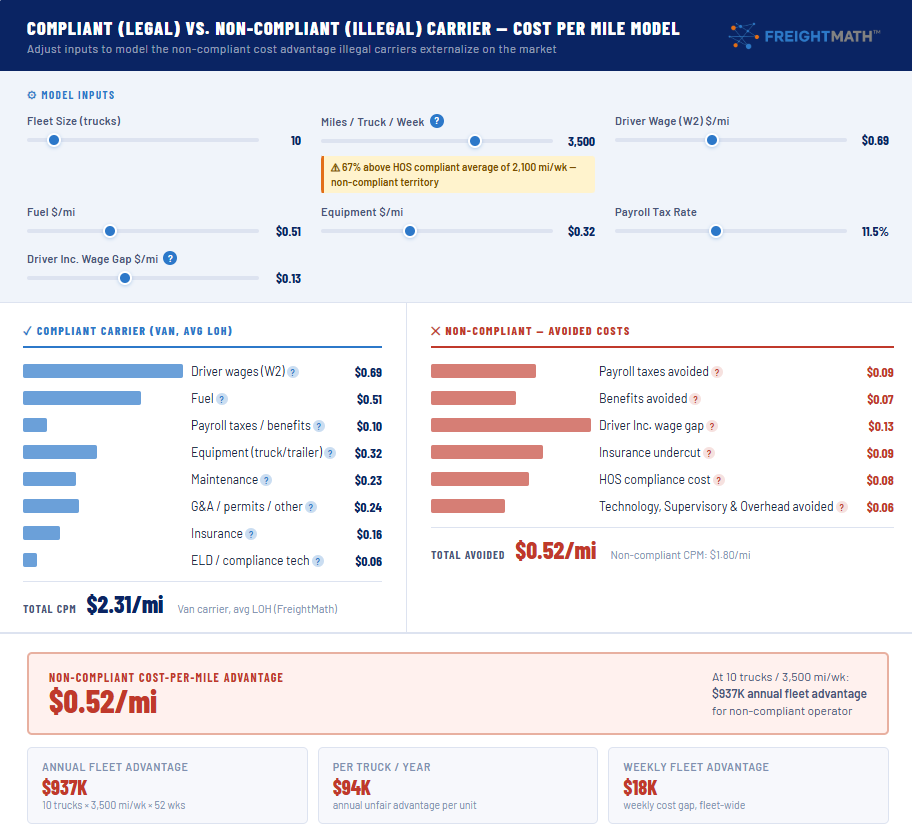

The competitive consequence is not subtle. Industry analysis describes a “two-platform market” that the ELD mandate was supposed to eliminate. Compliant carriers, operating within legal hours-of-service limits, run an average of 2,000 to 2,500 miles per week per truck.

Carriers using manipulated logs are running 3,500 to 5,000 miles per week. That difference in utilization compresses cost per mile so dramatically that a compliant carrier cannot match their rates and remain profitable.

At $2.38/mi for a compliant van carrier, versus an estimated $1.65/mi for an operator avoiding payroll taxes, benefits, insurance, and ELD compliance costs, the gap is $0.73 per mile. On a 10-truck fleet running 3,500 miles per week, that translates to over $1.3 million in annual cost advantage for the non-compliant operator. Freight rates are not just being undercut. They are being set by operators running on falsified safety records.

Click on image below to access the Carrier Cost Per Mile Model interactive calculator.

The scale of the problem forced a response. In 2025 alone, FMCSA revoked 42 non-compliant ELDs from its approved list and blocked 238 new applications from self-certifying, a 62% increase in annual revocations over the prior year. The agency overhauled its ELD vetting process entirely, implementing pre-publication review to catch fraudulent devices before they reach the registered list.

CVSA added ELD tampering to the North American Out-of-Service Criteria, effective April 1, 2026, making it grounds for an immediate 10-hour OOS order when inspectors confirm falsification. The agency identified and revoked devices tied to a coordinated ghost-driver scheme, the Triton Logistics case, in which an overseas operation managed phantom drivers for a U.S. carrier, a scheme that had already killed three people on I-64 in Virginia before federal action was taken.

The enforcement gap that remains is the absence of criminal accountability. Civil fines imposed after fatal crashes have been, in documented cases, roughly equivalent to the replacement cost of the truck involved.

Without criminal prosecution of the executives who direct ELD fraud schemes, the financial calculus remains one-sided. FMCSA has acknowledged the gap and has signaled that forthcoming rulemakings will include stronger vetting standards and end self-certification entirely. Until third-party certification becomes mandatory and criminal referral becomes routine for systematic log fraud, compliant carriers should continue documenting and reporting every instance of suspected ELD manipulation they encounter on the road.

The Self-Certification Problem: 40 ELDs to 1,100

When the ELD mandate took effect in 2017, roughly 40 devices appeared on the FMCSA registered list. Today that number exceeds 1,100. The technology did not advance at 30 times the pace of adoption.

The list grew because FMCSA permitted manufacturers to self-certify compliance with federal technical specifications – no independent testing laboratory, no government audit of device functionality, no meaningful barrier to re-registration after a prior device was revoked. Submitting a web form and checking a box was sufficient to appear on the approved list and begin selling into the market.

The result mirrors precisely what happened with CDL mills. Fraudulent driver training providers exploited state certification systems to issue commercial licenses to unqualified drivers – operators who had never sat in a truck, never backed a trailer, never executed a pre-trip inspection.

The credential looked legitimate because it passed through a government-sanctioned process. The process itself had been gamed. ELD self-certification is the same structural failure applied to hardware and software. The approved list signals legitimacy it cannot actually verify. A device manufacturer can satisfy every checkbox on the registration form and ship a product engineered from the ground up to falsify records.

The deeper problem is that software-based certification is inherently point-in-time. Code can always be modified. A device that passes a third-party audit on a Tuesday can receive a firmware update on Wednesday that restores the manipulation functionality that was temporarily disabled for testing. Even a rigorous independent laboratory assessment captures only the state of the device at the moment of review.

Until FMCSA implements continuous compliance monitoring with mandatory reporting of firmware versions, over-the-air update logs, and cryptographic attestation of device state at roadside inspection, third-party certification will face the same spoofing risk as self-certification, just with an additional layer of paperwork in between.

The CDL mill analogy holds here too: States issued credentials through an apparently valid process; the process had been compromised before the credential was ever issued. The approved ELD list is not a safety guarantee. It is a registration record.

What This Means for the Market Ahead

The carriers reading this article are, by definition, the ones who stayed in the game the right way. You carried proper insurance. You employed your drivers. You maintained your equipment. You paid your taxes. You hired to the full qualification standard, English proficiency included. You survived 13 quarters of margin compression while competing against operators who externalized every one of those costs onto the public, onto their drivers, and eventually onto the crash victims who paid the ultimate price.

The enforcement momentum building across North America is real, sustained, and accelerating on multiple fronts simultaneously. MOTUS is live and closing the front door on chameleon carrier registration. The SAFE Act is advancing through Congress. CRA inspection blitzes are underway. Budget 2025 funded a permanent Driver Inc. enforcement apparatus. ELP is now an out-of-service violation with real roadside teeth.

The non-domiciled CDL credentialing system is being overhauled from the ground up. More than 7,000 fraudulent CDL training providers have been removed from the federal registry. ELD tampering is now an immediate out-of-service trigger, 42 non-compliant devices have been pulled from the approved list, and self-certification is being replaced with genuine vetting.

These are not announcements or intentions. They are structural changes in the operating environment that are removing unqualified and non-compliant operators from the road every single day.

The combined effect is already visible in the capacity data. Spot rates are running materially higher year-over-year. The floor is rising, and for once, it is rising because operators who were pricing below cost through regulatory non-compliance are being systematically removed, not because demand happened to surge.

For compliant carriers, this is the moment the industry owed you. The regulatory floor you have always priced to is finally being enforced across the board. That changes the competitive math in your favor.

Make sure the regulators know legitimate carriers are watching, you support this work, and you will report what you see. The industry that emerges on the other side of this enforcement cycle will be smaller, safer, and, for those who ran clean operations, more profitable than the one we are leaving behind.

| REPORT ILLEGAL ACTIVITY – NORTH AMERICA |

|

| United States – FMCSA | Canada – Driver Inc. / ESDC and CRA |

| National Consumer Complaint Database: nccdb.fmcsa.dot.gov

Toll-free hotline (Mon-Fri, 8:00 a.m.-8:00 p.m. ET): 1-888-DOT-SAFT (1-888-368-7238) Report: chameleon carriers, unqualified drivers, ELP violations, safety violations, broker misconduct |

Labour Program Misclassification Reporting: canada.ca/en/employment-social-development

CRA Leads Program – T4A / tax fraud: canada.ca/en/revenue-agency (Leads Program) Tip line: 1-888-TIPS-811 Report: Driver Inc. operators, PSB misclassification |

For more information, please contact a KSMTA advisor via the form below.

Sources: ACT Research (Feb. 2026); FreightWaves/SONAR; FMCSA MOTUS program; FMCSA ELP enforcement guidance (May 2025); CVSA Out-of-Service Criteria updates (Jun. 2025, Apr. 2026); FMCSA non-domiciled CDL interim final rule (Sep. 2025); FMCSA ELD revocations and vetting overhaul (Dec. 2025); FreightWaves ELD fraud investigation (Nov. 2025); CVSA ELD tampering inspection bulletin 2026-02; FTR Transportation Intelligence (Oct. 2025); J.B. Hunt immigration policy analysis; Commercial Carrier Journal / TCA Truckload 2026; The Trucker (Dec. 2025); ATRI Operational Cost of Trucking 2024/2025; Canadian Trucking Alliance; Government of Canada Budget 2025; ESDC; CRA; Policy Options (Aug. 2025); CBC News (Jun. 2025);DOJ Antitrust Division HHI Guidelines (2023); ATA Economics Data (2025); Technavio North America Road Freight Report (2024); GAO chameleon carrier analysis.

Related Content

Where Ownership

Meets Opportunity

At KSM, you’re more than an employee, you’re a firm owner.